Smallholder farmers, especially in Kenya face difficulties when it comes to accessing loans and financing from banks and other financial institutions. The agricultural sector is the backbone to Kenya’s economy, yet banks have very little incentive to work with farmers.

Smallholder farmers, especially in Kenya face difficulties when it comes to accessing loans and financing from banks and other financial institutions. The agricultural sector is the backbone to Kenya’s economy, yet banks have very little incentive to work with farmers.

Financial institutions cite that the agricultural sector is a high risk sector and for this reason they shy off from offering loans. The fact that farmers don’t keep records of their sales, has done more harm than good in discouraging financial institutions from working with them.

To bridge this gap, FarmDrive founded in 2014 has built an innovative solution that provides “detailed risk profiles of smallholder farmers to financial institutions”. FarmDrive does this through a credit score, generated by an algorithm developed by the team, in-house. The algorithm relies on data-sets collected from the farmers through their mobile phones, alternative data and machine learning.

Mobile Phone Technology

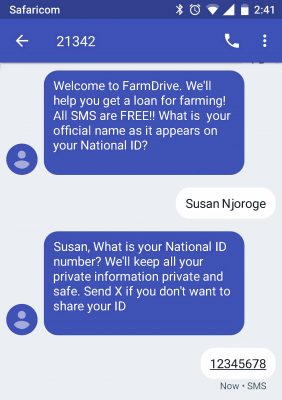

When farmers sign up to the platform, either by SMS or by using the app, they are asked a number of questions that will be used to create a farmer’s profile. The questions aim to find out the farmer’s location, crops cultivated, size of the farm and assets such as tractors.

FarmDrive also uses psychometric testing to determine a farmer’s character. Elvis Bando, Lead Data Scientist at FarmDrive says that this is necessary for them to have a proper profile of the person they are working with.

The farmers who qualify for loans, receive the loans via M-Pesa and also pay back the loans via the same platform.

Credit Scoring

FarmDrive’s algorithm is currently in its second stage. During the first phase (the pilot), which ran between December 2015 and December 2016, the company collected environmental data (weather and climate patterns, soil data) economic data (income, market data), social data such as social network information, including the apps usage and individual data, from the participating farmers.

The aggregated data is then fed into FarmDrive’s machine learning algorithm which generates credit scores, that will later on be used by financial institutions.

Throughout the pilot period, the company registered 3000 farmers spread across 16 counties in Kenya and disbursed 400 loans, amounting to over Ksh. 13 million with each loan averaging to Ksh. 33,000. During the pilot phase, FarmDrive was working with Musoni Kenya, a tech driven Micro Finance Institution (MFI) which provided the loans to the farmers.

Machine Learning

In its next phase of algorithm development, FarmDrive seeks to expand the environmental arm of the algorithm by incorporating more alternative data-sets, including satellite imagery and remote sensing data. They are currently engaging with Planet, a satellite company from Silicone Valley, and The Impact Lab, a Chicago-based data analytics firm to analyze the possibilities of using satellite images in predicting a farmer’s creditworthiness.

In addition, FarmDrive also plans to use these environmental data-sets, in combination with crop cycle data to predict seasonal yield and influence agricultural insurance products.

The startup also uses machine learning in generating the farmer’s profile by learning from the farmer’s input. Data points about the farmer’s behaviour, education level, and their interaction with the app are all analyzed to contribute to the farmers profile score.

The Future

Jokingly, Mary Joseph, FarmDrive’s director of partnerships and external relations, said that they might not know what they will be doing in 5 years since the company is still in its growth stage, however they do plan to use the data collected to offer economic advise, up-to-date data, and pre-process data to financial institutions and other stake holders trying to drive solutions to farmers.

{kind=link}